|

|

Blog |

|

All businesses whether large or small and regardless of the industry have one thing in common, they all have customers. For many small businesses most clients are a one time interaction where the customer pays in full, but what about the clients that purchase on account from you? Customers more than anyone have a huge impact on cash flow and a recent Manta survey found that the number one concern that keeps small business owners up at night is money and finances at 35% followed at a distant second by competition at 11%.

With clients that are on account you are providing goods and services but will not see payment until a later date. Having a good accounts receivable system or process is crucial. If you think accurate customer balance information is a pain point only for small businesses you would be surprised. I worked for a Fortune 500 and we regularly ran into accounts that were incorrect because they were billed incorrectly or the payment was applied to an incorrect customer. A good receivable or billing system should allow for individual customer account activity. You should use invoices that allow you to record individual goods or services to list out what is being provided. If you use accounting software make sure to set up the list of goods and services and keep them updated so that you select them to add to the invoice which makes the process faster. You can then also run a reports later to help with merchandise purchasing decisions (more of product A and less of product B). Brand your invoices with your business name or logo to give a professional look to them and make sure that they state when the bill is due or any discounts for early payment. Make sure your contact information and online payment portal are listed so customers can easily call or go online to make payments. Unless you only have a handful of customers use account numbers to ensure that payments are posted to the correct account. If a client hasn't paid in a while you should apply the payment to the oldest invoice(s). Have a cutoff date for getting all invoices and payments into the receivable system (usually end of month is a good time). Once all invoices and payments have been entered you can run aging/accounts receivable reports. Accuracy of data entry is crucial for these reports. You don't want to send a paying customer a letter telling them their behind on their payments. The aging report can be a very effective tool to find out which clients are paying on time and which are not and help determine whether or not to continue to do business with specific customers. Make sure that the date settings on the report are correct and reflect your businesses billing terms. Once you have your aging report you can look to determine which clients are over 60 days and over 90 days and reach out to them for payment or to set up a payment arrangements. Ensuring you have an effective receivable/billing system and processes will let you know which customers are current and which customers have fallen behind, will help better manage your cash flow which is critical to smaller businesses and maybe even a better nights sleep. Thanks for your interest and we hope to continue to have meaningful conversations.

0 Comments

Having financial controls is important to any business whether large or small. For smaller businesses this is a challenge since some have only a few employees and many of the financial actions are handled by the owner.

But what financial controls can you implement that are relevant for your small business? Having a safe or a file cabinet that locks is good for keeping items such as your businesses checkbook, cash or check receipts from clients or items such as your credit/debit card processing attachments that plug into your phone or tablet. It is also good to keep documents that may have sensitive information like your bank account number or your card number. Documentation is important. Keep receipts and deposit slips and always compare to bank statements or review your accounts online. This ensures that you catch any discrepancies in deposits that are posted and that you catch any fraud on your account before it causes too much damage. Reviewing your accounts at least twice a month is a good idea. Deposits should be taken once or twice a day. If you should receive additional client payments after a deposit run or receive them late in the day, place them in the safe or locking file cabinet. This ensures that cash or checks are not lying around or on your person which could endanger your safety. Information security, this is new but just as important. Make sure to use strong passwords for online accounts like banking or credit card. (You should have strong passwords for all of your online accounts) Do not write down passwords and leave them at your computer (like under your keyboard). Use password housing applications and software to store that information. This will help since you will only need to remember one password. Never click on links from emails stating you need to reset your password, these are phishing emails. If you have any concerns always type the web address of your financial institution and access your accounts from there. As your small business grows you can add additional actions, like separation of duties and securing your private network. Increasing reviews and audits also becomes important as your grow since fraud is harder to spot when there is more activity in accounts. While these are just a few actions you can take, they are important and will lay the foundation and create the culture your small business needs to ensure that you have strong financial controls now and in the future. Thanks for your interest and we hope to continue to have meaningful conversations. What is a full year forecast? Isn't that basically a budget? These are actually two very different tools that businesses can use. In larger organizations both are used and the organization and it's leaders are measured on how close actual results are to budgets. Larger organizations also have dedicated employees or even an entire team that build budgets and analyze, calculate to provide monthly forecasts.

We know that budgets are your businesses plan for the following year and are built at a more detail level. It's a strategic tool to help determine what needs to happen to meet any kind of goals you may have. You want to increase sales or start a new line of business? You can budget this out to find out what drivers you need to impact and how to impact them. The one issue with budgets is that environments that we operate in can change dramatically at any moment and it can impact the rest of the year. Larger organizations will re-budget in the middle of the year to bring budgets in line with what is actually happening. Full year forecasts take your actual results year to date and project out the rest of the year. As you update each month with the actual results you re-forecast major line items out the rest of the year based on what is happening. Re-forecasting can be done monthly or quarterly. It gives you an idea as to where you will land on the last day of the year. Forecasts are tactical tools and for helping address short term items. There is no variance analysis to forecasts as there are to budgets. Is one better than the other? With business environments changing as quickly as they are there is no question that a forecast is a more effective tool in seeing the future impact of current events. If your forecast is showing that your revenue or sales will decline, you can take immediate action to address this. If your actual is lagging behind your budget it may do this for the rest of the year and your variance will get larger. There is a risk that at some point in the year, the budget becomes irrelevant to decision making. Also since forecasts have you re-evaluate major items it provides you with the opportunity to see how different initiates are impacting your business giving you the ability to adjust and tune how you run the business to find the right mix for success. As with budgeting, the process for forecasting can be based on trends and percentages and be adjusted up or down to match what is happening. In the end, forecasts can be a good tool for making course corrections for your small business ensuring you avoid declines and that your year end results are not a surprise to you. So you have been reading our emails. Your taking your finances seriously, you are making sure that your expenses are being booked to the correct accounts and are closing the books. Now you have a set of freshly printed financials sitting in front of, and now your thinking "Ok Alex, now what?"

Reading financials is like knowing how to read another language. While making sure that the last number at the bottom of a financial statement is black or without parenthesis (notating a loss) it's not the only aspect to look at. An Income Statement is a snapshot in time. It shows you how you did for the month, year or year to date by showing how much income came in during the time period and how much it cost to generate that income. The best time frames to review are the previous month and year to date. Why both? It represents a tactical and strategic view of your business. Reviewing the previous month can let you know if any issues have come up that need to be investigated and addressed. You should always take into consideration any seasonality or peaks and valleys that occur throughout the year especially if your business is driven by weather or seasons. Any strategic or long term business decisions should be based on your year to date. In essence when you review your financials you should look to see how the current month contributes to your year to date, you don't want to rewire your entire business due to one off month. There are also some calculations that can be used to help know how well your business did. Gross profit margin can let you know how much of the income you were able to keep after expenses. Calculating the percentage that an expense item is to total revenue is good to know which expense line item is the highest. You can also compare your financial statement to a budget if you have one to see how close you came to expectations. Comparing current month to previous month or to the same month from the prior year can also be good ways to measure how well your business is doing. Some other calculations you can perform are average revenue per client or comparing sales volumes to budget or other periods. This allows for a holistic view and incorporates operational volumes. While it is tempting to look at expenses and to see what can be eliminated in terms of costs, it is not the only part of the business that should be scrutinized. Yes, a business should run as lean as possible but instead of cutting costs, look to increase the value your getting for your business dollar. Also look to see if your advertising costs are providing you the sales you need for your business. There needs to be a balanced approach where both sales and costs are reviewed for opportunities. Avoid the mistake of trying to make your business succeed from the expense side of the income statement only. So knowing how to read your income statement will provide you a wealth of knowledge of not just what is going on with your business but also what opportunities there are for your business to be more successful. With knowledge comes power, the power for better decision making and driving success. Month end close, what is it and why is it important? This is a process that is carried out by accountants and bookkeepers where the books are closed or properly wrapped up. The reason it is important because it provides data and information to create financial reports that can help business owners and managers make smarter business decisions. If all items are not recorded and not recorded in their correct categories financial reporting is inaccurate and becomes irrelevant to the business manager or owner. Another reason it is important? You know where your business stands as opposed to going a whole year and learning your business had a loss. This allows you to make adjustments and correct any issues so that they don't linger all year.

The process of month end close requires gathering all information and transactions that have occurred during the month. Depending on whether a business uses accrual or cash basis dictates how transactions are recorded and how they are presented in reporting. Receipts for items such as inventory, travel expenses, meals, office supplies, etc. are gathered and recorded not just to the correct month, but to the correct expense line item or balance sheet account and if necessary the correct line of business. Another reason that properly recording expenses are important is due to the tax benefits some business expense items have. Journal entries have to be made as well recognizing transactions such as payroll expenses. Once all transactions have been accounted for and recorded. Then accountants and bookkeepers run certain reports to ensure that all accounts are in balance. Once this is done financial statements and balance sheets are run and can be presented. In some organizations financial analysis is performed with ratios, volume/rate analysis, to help determine what is going on in the business. With the increasing development of decision science and the marrying of operational and financial data new analysis and insights are being brought forth that go far beyond just whether there is a net profit or net loss. This kind of analysis gives a holistic view of the business and emphasis on what is referred to as business drivers. Business drivers are defined as the crucial factors that are vital to the continued success of your business. It isn't just sales but factors that impact operations and sales. As we can see month end close and the accurate recording of business expenses provides the foundation for accurate, actionable reporting and analysis that can provide business managers and owners with the necessary tools and information to make better business decisions. Recently I met a young man who does marketing and works to promote female entrepreneurs. Invariably I checked out the website and Facebook page. There was an article about the 7 things that a a small start up or small business should do. For the most part it was a good article (although it did state that you should always pay top dollar for marketing) but I was shocked when it came to finance it stated that if you can't find a financial guru "just find someone who can manage money". This is irresponsible, dollars are the life blood of any business and the odds are already against small businesses.

Financial experts are no longer scorekeepers, they are a CEO's strategic partner responsible for helping determine the drivers for the business, how best to measure them and provide decision support. The world of finances has moved beyond counting cash and taxes and require analytics and decision science. Operations are heavily reflected in financial activity. Financial experts can interpret results and help the CEO develop overall strategy as it relates to the business. A financial expert or business manager can also help navigate a small firm as it starts out. All data continues to show that small businesses fail and that many of the reasons is related to finances. Small business stats: 1) There are almost 28 million small businesses in the US and over 22 million are self employed 2) Over 50% of the working population work in small businesses 3) About 543,000 new businesses start each month but right now more businesses shut down than start up 4) 7 out of 10 firms survive the first two years, half survive five years, a third survive ten years and only a quarter survive over 15 years 5) Number one reason businesses fail is because they run out of money Research from the 2013 Global Entrepreneurship Monitor report which was produced by Babson College and other universities found that the top reasons for businesses closing in the U.S. were problems related to financing and lack of profitability, these were cited in more than half of businesses that closed. This is the reason why a financial expert is crucial for small firms and start-ups. While we can understand that finances are not as sexy as marketing there is nothing sexy about bankruptcy or failure. Small businesses need a good strong team. While your marketer is responsible for crafting your message and telling the story of your small business a financial expert will help you navigate your small firm or start up through the dangerous waters. Consider these questions: Do you know your burn rate? What is your break-even point? How much cash or time do you need before you get there? How much operating cash do you have on hand now if your business had to stop operations and how many days would that cash last? How much revenue is your marketing generating? Not how many click or 'Likes', while these can sound impressive ask what percent of clicks and likes become paying customers. Someone who can only manage money can't give you that information. Do the questions give you pause as a small business owner? They should. The answer to these questions can mean the difference between success and failure. A financial expert, a guru, can help your small firm from becoming another data point in the vast records of closed businesses. The recent hack of Sony's systems have been in the news like so many other hacks. What makes this one different is the information that has been made available. While other hacks were about national security or personal debit or credit card information, this hack stems from a movie that Sony produced. The emails that have been released have been perhaps the most damaging since they contain personal opinions and commentary from everyone at Sony up to it's executive leaders about actors and even the President.

One would say that smaller businesses are more vulnerable since they may not have IT security measures or software like Sony so all of their information could be attained by a novice hacker. There are a couple of lessons from all of this. 1) Business emails should be all business. Because the line has blurred between our personal and professional lives we may get complacent and mix our content with our communication channels. Never add personal thoughts about others like coworkers, vendors, competitors or clients. Remember also that emails can be admissible in court for cases such as slander. In this case it's best to follow your mom's advice, 'if you can't say something nice about someone...' 2) Be selective when emailing. Remember, an email travels along a long path passing many different servers and equipment before reaching it's intended audience. Google, Microsoft and ISP's are always scanning emails for marketing opportunities so hackers may be able to as well. If a phone call or face to face would be appropriate for the information that needs to be relayed use those channels instead. 3) Have a policy or rules for emails. Setting up some rules about the appropriate use of email in a work setting is good especially if you have employees. If you are a sole proprietor or smaller organization make sure to keep your business and personal communications separate and be mindful of the information you transmit. 4) Most importantly, never ever click on links in emails that appear suspicious from unknown persons or vendors/clients. Hackers are getting more and more sophisticated with this process. They will send an email with malware that will collect your contacts and email them so your contacts believe they are getting an email from you when in reality they are getting an email from the hacker. Always check the address that it is coming from since this can be a dead give away (ex. the name display is John Smith from ABC Company but the address is jdoe@hack.com) As always, if you know the person and are not sure about the email you can call them to verify whether it is legitimate or not. While it appears that anyone can be hacked, keeping business emails, business can help prevent alienating others around you, damaging your small businesses reputation or brand or opening your or your small business to slander and defamation. Change is inevitable, nothing remains constant. This year has been a year of many changes for me personally. I proposed to my fiance, I lost my father, we made some changes in our firm to better manage or be more efficient. There is nothing we can do to stop change, but we can take steps to manage those changes.

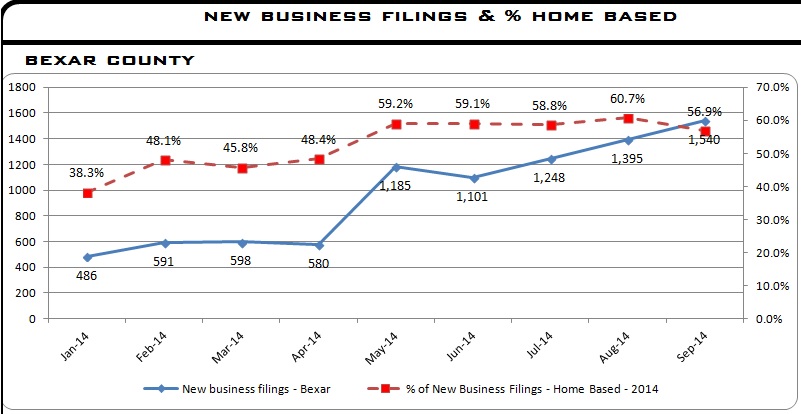

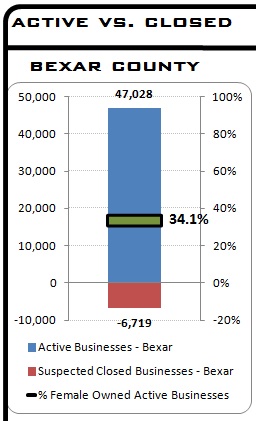

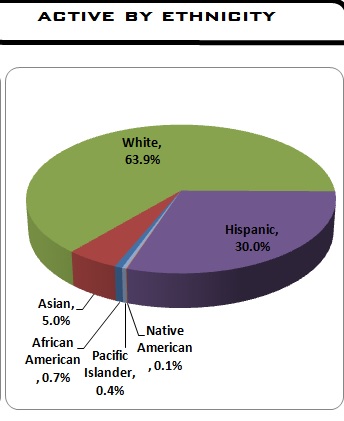

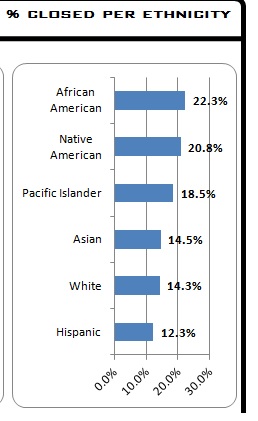

There is a whole specialty and management philosophy known as Change Management. It is usually part of project management and has to do with dealing with the aspects of implementing changes. The reasons that could be driving change can be external or internal to the firm. It can be changes in the industry or changes such as technology or the advent of social media that can create the need to change to keep up or remain relevant in the new environment. To effectively manage change there are four steps within the process: 1) Recognizing changes in the business environment (industry, media, technology, etc.) 2) Develop adjustments to meet the companies needs 3) Communicating, training employees to the coming changes 4) Buy in from everyone in the company There are other factors that can impact how much effort it may take to carry out change like how ingrained is the culture? Are leaders committed to the changes? Does the firm or organization have the capacity to adapt to the changes and will adapting changes bring about the desired outcomes or meet the business needs? Successful change management will be efforts where: 1) The benefits and changes are effectively communicated to stakeholders and employees 2) Employees are provided effective education & training 3) Fears and resistance effectively countered through communication, vision and training 4) Changes are monitored for fine tuning and adjustments While we cannot stop changes, we can take steps to better manage how changes impact our small businesses. One of our capabilities is dashboard development. What is a dashboard? It is a high level report that provides key performance indicators and is limited to summaries, key trends or comparisons. This tool allows owners or managers to see at a glance what direction their business is going in or if there are issues. The term dashboard comes from the automobile dashboard where drivers can monitor the various aspects of the cars operations via a cluster of instruments in one location. Four essential elements for a good dashboard are: 1) Easily communicates information 2) Has minimum number of distractions 3) Supports the business with meaningful or actionable data or information 4) Utilizes human visual perception, visually communicates information Dashboards can be utilized by any area of the business such as sales, operations or finance. A dashboard for the entire business or all operations can be created showing key indicators for each of the functional areas as well. As with any report, knowing who the audience or the consumer of the information (sales manager, finance director or CEO) will help in knowing what information or view is needed. We recently created a dashboard that has data in regards to new business filings and currently active businesses. We used data from RefUSA. We included all new business filings and for active businesses we used registered and verified businesses with less than one million in revenue and less than five employees. Below are a few screenshots of sections of the dashboard. As we can see the information gives us a good view of smaller businesses in Bexar County. From above we now know that new business files in Bexar County have been steadily increasing since May. The percent of home based new business filings has also been more than 50% since May as well. We know that there are 47,028 verified active businesses and that 34% are female owned businesses. The one aspect that stands out is that even though 30% of registered businesses are Hispanic owned, as an ethnicity Hispanics in Bexar County are more successful in keeping their businesses open (only 12.3% closed) while African Americans in Bexar County face greater challenges (22.3% closed). (To see the full Small Business Dashboard with info for Texas and the US click on the pdf link in our Business Counts section or visit the newsletter tab on our website) Dashboard design is almost like a fingerprint, each one is unique and is driven by the needs of the business and what the business feels are the most important aspects that should be measured. You can't use a cookie cutter approach and apply a template to different businesses. Knowing what drives your business and how best to measure it will aid in designing a dashboard for your small business. I recently was on a LinkedIn forum for CFO's and a question was raised, 'what has more bottom line teeth, revenues or expenses?' There were many great responses and feedback from seasoned financial officers but the consensus was that you have to address the impact of both and pursue a balanced approach.

There has been in the last few years an inclination to look only at reducing the expenses to increase the bottom line. Many large corporations have been looking at ways to continuously reduce costs. But you have to take a realistic look at your expenses. If your expenses are large or bloated then yes you will definitely need to review expenses to see where you can make improvements, but you don't want to cut into muscle and cripple your business. There are some expenses that are necessary for your business to exist. These fixed costs cannot go away or be made to disappear. Also each new client creates an incremental increase in operating costs, there is no way to increase revenue without a corresponding increase in expenses. Financial officers always look to and try to contain costs because it is the part of the business that they understand and can control. Revenue is a product of sales and in larger organizations is handled by a sales team or a larger marketing organization. But to manage both effectively you need information and analysis. What percent is your fixed costs and variable costs to your revenues? Is this percent consistent month to month? What is your revenue per client or product? How much of that revenue per product is going towards fixed costs and variable costs? Are your costs per product or client even with or higher than your revenue per product or client? A pricing model can be critical because it forces one to account for fixed costs and the variable costs that you have for each client you service or widget you produce. Once you have this information it can also help to determine the minimum sales you need to break even. Any sales plan that goes below this will mean losses for the business. With knowledge of what the incremental cost per client or product is you can forecast out the increase in costs for each benchmark in sales. This lets you know what your max capacity is and at what sales level you would need invest in assets or equipment to take on more sales. As your sales increase make sure that your percent of expense to revenue stays consistent, wild or erratic changes in percentages should be reviewed. As with all things, a balanced approach is the best way and constantly reviewing opportunities for improvements for both your revenues and expenses have the biggest bite to your bottom line. |

Archives

November 2020

Categories

All

|

RSS Feed

RSS Feed